Black Knight, it the current edition of its Mortgage Monitor covering December mortgage performance data, writes an epitaph for slowing home price appreciation. Prices had been appreciating at an annual rate of nearly 7 percent in early 2018 but had fallen to 3.8 percent in August of 2019 as affordability worsened.

But then, as Black Knight's President of Data & Analytics, President Ben Graboske writes, "The national home-price-growth rate gained a good deal of steam as mortgage interest rates declined throughout the second half of last year. In fact, December marked four consecutive months of home price growth acceleration and the largest single-month acceleration in more than 6.5 years, while the annual rate of appreciation saw nearly a full percentage point increase over the last four months of 2019, closing out the year at 4.7 percent."

Much of the month's Monitor is concerned not only with how these lower interest rates throughout the back half of last year contributed to sharply accelerating home price growth, but also to improving affordability.

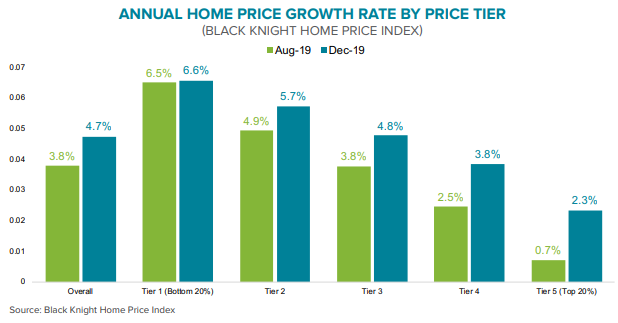

At the low end of the market, those homes in the bottom 20 percent by price, continue to grow at nearly three times the rate of those in the top 20 percent price tier; 6.6 percent versus 2.3 percent in the last four months of 2019. However, that highest priced tier has been more reactive to the recent declines in interest rates; the rate of appreciation among those homes nearly tripled from August to December while the bottom tier barely budged.

Reactivity has also been geographic. In New York City the end-of-year growth rate jumped 80 percent. Some of the West Coast metro areas where the rate of price increases had been plummeting into negative territory have turned around as well. Increases in both San Francisco and San Jose have bumped 4 points higher and Seattle went from an 0.7 percent rate mid-year to 6.1 percent, higher than the national average.

The bi-coastal volatility doesn't apply everywhere, however; growth rates in general have become more uniform across the country. Salt Lake City tops the list of metro areas with an 8.1 percent rate of increase, but this was the lowest maximum since 2011. More than 60 percent of markets were appreciating at rates in a narrow band between 3 and 6 percent.

But, despite the average home price increasing by nearly $13,000 from just over a year ago, the monthly mortgage payment required to buy that same home has actually dropped by 10 percent due to falling interest rates

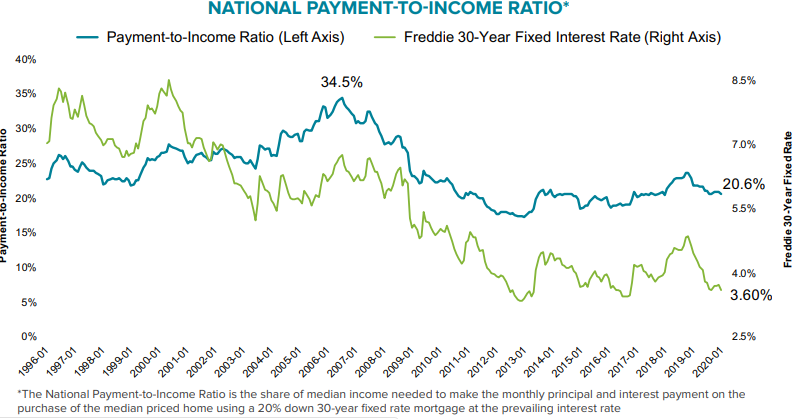

"Still, even with home price growth accelerating today's low-interest-rate environment has made home affordability the best it's been since early 2018, Graboske points out. "At that time, the housing market was red-hot, with national home price growth at 6.6 percent and climbing - before rising rates and tightening affordability triggered a pullback in growth rates. That's not the case today. Despite the average home price increasing by nearly $13,000 from just over a year ago, the monthly mortgage payment required to buy that same home has actually dropped by 10 percent over that same span due to falling interest rates."

The median monthly income that is now required to purchase a home is now 20.6 percent, the smallest payment-to-income ratio in two years. In contrast that ratio was almost 35 percent at the height of the housing boom. This means that a homebuyer could purchase a home costing $48,000 more than they could have bought at the same time last year with the same monthly principal and interest payment. This is a 16 percent increase in buying power.

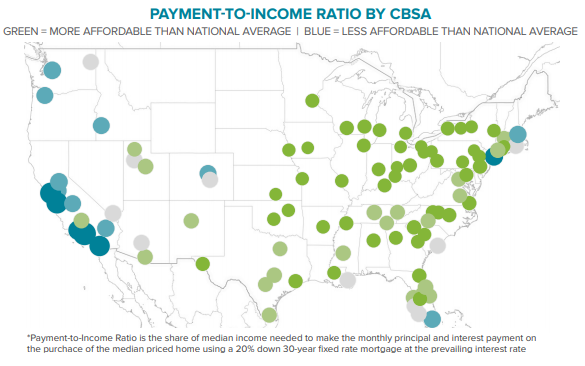

In late 2018 when rates were in the mid-to-high 4 percent range, purchasing a home was less affordable than long-term averages in nine states and the District of Colombia. This week only California and Hawaii remain on that list. Unfortunately, in the past, comparable levels of affordability have put upward pressure on home prices.

The recent decline in rates has also restored an incentive to refinance to a large chunk of homeowners. Rates fell to 3.6 percent during the week ended January 23 according to Freddie Mac's weekly Mortgage Market Survey so Black Knight took an updated look at the pool of homeowners who might refinance a mortgage.

The company defines that pool as those with a 30-year mortgage in good standing, at least 20 percent equity in their homes, a credit score of 720 or higher, and the ability to shave 75 basis points off of their current interest rates with a refi. As of January 23rd, there were 9.4 million such homeowners, the largest pool since last October when interest rates briefly fell below 3.6 percent. (As an aside, Freddie Mac's rate fell another 9 basis points after this calculation was made.)

On average, these borrowers could save $264 per month, for an aggregate monthly savings of nearly $2.5 billion. While down slightly from the $2.6 billion aggregate potential savings in August and September of 2019, it is three times the volume of savings available at the beginning of last year. More than 2.6 million of these homeowners could save $300 or more on their monthly payments.

Black Knight points out that the qualifying requirements it uses in determining the size of the refinance pool is conservative. If only current mortgage specifications are considered, there could be as many as 19 million homeowners who could save those 75-basis points by refinancing.