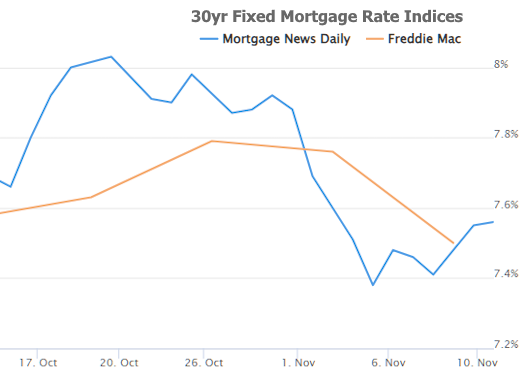

While it's possible to accuse mortgage rates of experiencing volatility over the past few days, this week was exceptionally calm compared to last week. So "everything's relative," and relatively speaking, that's a win.

Here's a snapshot of the action as told by 10yr Treasury yields, which tend to be moving in the same direction as mortgage rates:

As the chart points out, Thursday's 30yr bond auction brought this week's only instance of excess volatility. This refers to The Treasury Department's regularly scheduled auctions of US debt--some of the only interesting items on this week's event calendar as far as rates were concerned.

In general, Treasuries are the tour guides for the bonds that drive mortgage rates (MBS or mortgage-backed securities). They tend to hang out closer to the tour bus while MBS go off in search of adventure, but everyone is generally moving to the same places at the same time.

In other words, a big, volatile jump in Treasury yields often suggests the same for mortgage rates. Fortunately, this particular jump wasn't that big, and the 30yr Treasury bond is less correlated with mortgage rates than 5 or 10yr Treasuries. The result was only a modest increase in rates on Thursday and not one that erased too much of the recent improvements.

Of course we should remember that everything's relative...

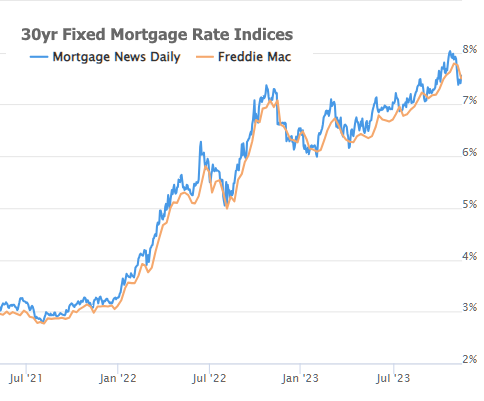

The chart above is not intended to rain on any parades, but merely to put them in context. It shows 3 previous instances of rates appearing to top out and push back against long term highs only to be persistently dragged higher. All that to say: it's promising to see rates mostly holding last week's improvement, but as far as long journeys go, it's best viewed a solid first few steps.

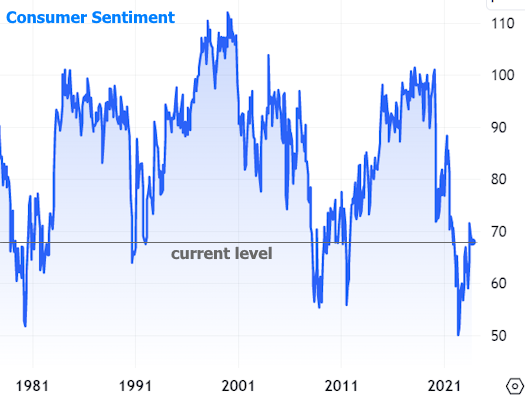

In order to continue the journey, the bond market (which dictates rates) will need to see the same things it's been wanting to see: lower inflation, softer economic data, and for the Federal Reserve to be seeing the same things. This week was very light with respect to data--especially inflation data--but there was an anecdotal mixed bag on Friday in the form of the Consumer Sentiment Survey.

Consumers were more downbeat overall with the sentiment index falling to 60.4 from 63.8 previously. This is LOW territory--not as low as we've seen recently, but nonetheless in line with some of the worse levels in more than 10 years.

In and of itself, low sentiment would be good for rates because downbeat economic data tends to suggest slower growth and lower inflation. But if inflation expectations are contributing to the pessimism, it cancels out the good news for rates. Incidentally, the same survey has an "inflation expectations" component for both 1yr and 5yr time frames. The 5yr is fairly boring, but here's the 1yr:

Consumers aren't crystal balls, but the Fed does consider consumer inflation expectations in its assessment of inflation. Fortunately, this isn't the only place they look for that data and Fed Chair Powell has recently mentioned that other indicators of inflation expectations are showing much more promise. Beyond that, this data series tends to be overly-correlated with fuel prices (although there is an odd and notable divergence from that trend at the moment):

Ultimately, consumer inflation expectations are a sideshow compared to the top tier inflation data. The Consumer Price Index (CPI), for example, has proven capable of rocking the rate market more than almost any other economic report apart from the jobs report. And we won't have to wait long for the next installment (this upcoming Tuesday).

The Fed has been clear and we should take them at their word that rates could be done moving higher if inflation and growth continue to cool, but that rates could easily move right back up if the data surprises to the upside.