The return of Americans to urban living, while well documented, may be a "head-fake" as far as the mortgage industry is concerned. Sam Khater, CoreLogic's Deputy Chief Economist says that inbound migration is happening, but not precisely in the way many think. This return to the cities has been driven by educated and affluent households, he says, which is leading to a concentration of wealth in cities and inner suburbs and that is driving home prices higher.

CoreLogic looked at the 20 largest MSA's, dividing the suburban areas in each into three equally weighted rings based on the percent of residential properties. This allowed an analysis where rings could be "fluid and expansive" in sprawling areas like Houston but small and compact in smaller, denser markets.

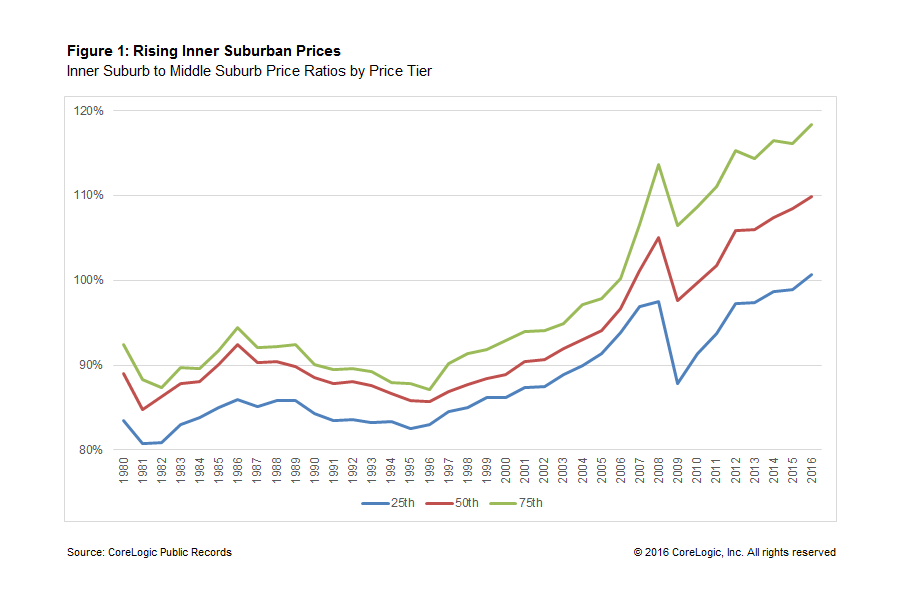

During the last two decades of the 20th Century middle ring suburban home prices were between 10 and 20 percent lower than those in the city itself and in its inner suburb ring. However, since the early 2000s, when the urban rebound first started, prices in the inner suburb have soared compared to what was happening in the middle ones.

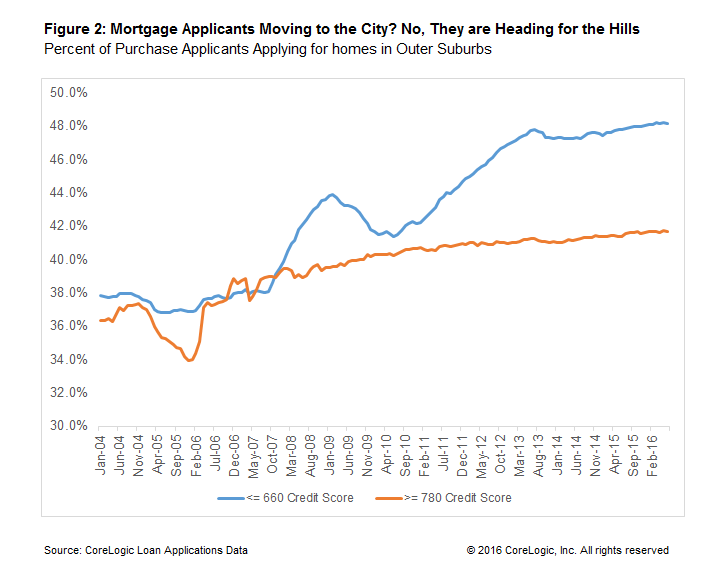

Consequently, there has been a countervailing trend for purchase mortgage applicants, especially lower credit borrowers, to seek affordability further out into the suburbs. During the housing boom in the mid-2000s, 38 percent of low credit purchase mortgage borrowers applied for loans in the outer suburbs. This shift continued even into the recession and by the fall of 2008 the percentage of lower credit borrowers in the outer suburbs reached 44 percent.

In mid-2010 that percentage declined and Khater attributes that to the temporary first-time homebuyer tax credit which allowed some borrowers to move closer in than they otherwise could. After that tax credit expired, the shift to the outer suburbs resumed.

By the middle of this year the percentage of lower credit purchase applicants applying in the outer suburbs was up to 48 percent, the highest since CoreLogic started tracking the phenomenon. Higher credit borrowers are also increasingly applying in those outlying areas, but the gain in that cohort is less than half that of lower credit borrowers and "there is a clear sorting of lower credit and income borrowers to the outer suburbs."

Khater, who was writing in the company's Insights blog, says this "increased sorting has economic and policy implications for spatial risk and increased concentration of lower credit borrowers in America's outer suburbs."