In order to make the most of today's newsletter, you'll need a basic understanding of the Fed Funds Rate (the thing the Fed actually hikes or cuts in an attempt to keep inflation in a target range) and the fact that mortgage rates are very different from the Fed Funds Rate.

Here is a handy primer that lays out all the reasons for that in reasonably plain language: No, The Fed Hike Doesn't Mean Anything For Mortgage Rates

Now back to the hope and the drama!

At the close of business on Wednesday, after another big rate hike from the Fed (as expected), there was hope that we would finally see a shift in recent trends in mortgage rates.

Wednesday's hope stemmed from a combination of factors. Rates had been rising quickly since the beginning of August, but accelerated to a troubling pace after last week's Consumer Price Index (CPI) release--a key inflation report that guides decisions of the Fed.

CPI did extra damage both because it was much higher than expected and because it happened so close to this week's scheduled Fed announcement. A similar scenario had played out in June, resulting in the biggest 3-day jump in mortgage rates in decades.

In other words, high inflation spooked the market into thinking the Fed would signal an even firmer commitment to its rate hike outlook. Not only did that happen, but in the Fed's forecast summary, there was a strong shift in expectations toward even higher rates in the coming months and years.

Granted, the members of the Fed can't begin to guarantee or even reasonably predict that rates will be as high in 2023-2025 as Wednesday's forecasts suggested, but if they had to guess at those levels based on what they know today, those are their guesses. Fed Chair Powell has repeatedly reminded traders not to put too much stock in those rate forecasts, but to no avail.

The average Fed member sees the Fed Funds Rate a full 1.0% higher by the end of 2023 than they did when the last batch of forecasts came out in June.

For anyone who doubted the disconnect between the Fed Funds Rate and mortgage rates, we can pause here to consider the following:

- The Fed Funds Rate is now 0.75% higher than it was when the last forecasts came out on June 14th

- The highest median forecast among Fed members is now 1.0% higher than it was on June 14th.

- And despite all that, Wednesday's mortgage rates were nowhere near 1.0% higher. They were actually much closer to June's levels.

And THAT'S the source of the hope. Or at least it was, as of Wednesday afternoon.

In other words, the market made it through what seemed to be bad news for rates from the Fed with rates actually moving a bit lower! The more optimistic hope was that such a ground-holding event could serve as a turning point in a brutal march to the highest levels in 14 years.

But everything changed on Thursday. The bond market had massive second thoughts about Wednesday's resilience. The underlying reasons for this remain a matter of debate among market participants, but we can see at least one piece of evidence that overseas bond markets played a role.

Specifically, bonds in the UK got destroyed in the 2nd half of the week for reasons esoteric enough that we won't even attempt to discuss them beyond saying it had to do with the confluence of a new budgetary announcement affecting UK bond supply and the as-expected announcement of bond sales by the Bank of England.

Ultimately, you don't really need to understand the details as much as you need to see how different the movement was between US and UK 10yr government debt (the quintessential benchmark for longer term interest rates in their respective countries). The following chart shows how much each 10yr rate has moved this week:

The discrepancy here is hard to overstate or over-appreciate. This is an absolutely massive liquidation in a market that always has some measure of spillover onto rates in the US. In other words, we very likely would not have seen US rates shoot higher nearly as quickly if not for the goings-on in the UK bond market on Thursday.

Therein lies our new hope. It's not a forecast or a prediction--just a glimmer. UK rates jumped even faster on Friday and US rates paid even less attention. All other things being equal, this could be seen as a sign that traders in the US are finally sensing some exhaustion in what has certainly been an exhaustive effort to push rates higher over the past 2 months.

For the record, we're talking about 10yr government bonds because mortgage rates correlate very well with government bonds and government bonds give us a far superior way to compare rate momentum between these two countries.

Also for the record, rates are still really high, and the rate landscape is a relative mess. In fact, there's no perfect way to relay the current position of the top tier 30yr fixed rate because it varies greatly depending on the lender's pricing structure and the borrower's pricing preferences. The big issue is the presence of upfront costs. They're unavoidable in many cases. In others, lenders use them to offer clients a way to "buy down" to a lower rate.

To be sure, while "points" or "buydowns" aren't good or bad, they are an interest expense in the same way the interest portion of your mortgage payment is. You're just paying it upfront instead of over time.

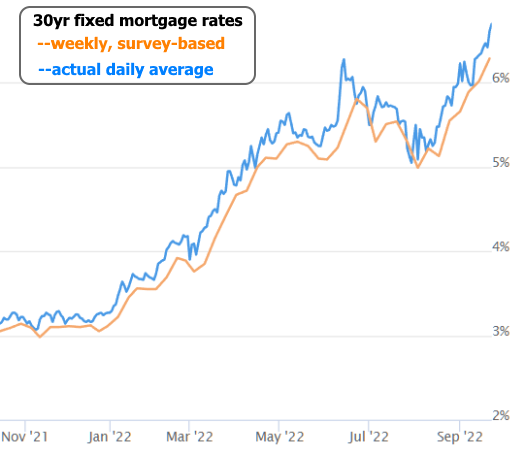

All that to say that the rates appearing in many news headlines are hopelessly low. Freddie Mac's weekly rate survey just came out at 6.29% on Thursday. Not only does that require almost a full "point" of upfront cost, it's also very stale data at this point. If we could magically remove the mortgage market's ability to rely on points as a part of the rate quote equation, the average lender is now much closer to 7% than 6.29% based on actual daily rate offerings analyzed right up through Friday afternoon.

While it is true that the pain of higher rates is the pain the Fed wants us to feel in order to fight inflation, the market may soon sense that the Fed has done enough to accomplish the desired shift, even if the Fed isn't as quick to admit it. It's definitely noble to fight inflation, and as the Fed says, it's definitely dangerous to do "too little" to fight it. But it's also true that mortgage rates near 7% are already doing plenty to fight home price inflation. If the Fed begins to think 7% rates would do "enough," today's glimmer of hope will increasingly prove to be justified. Otherwise, rates will continue up and over 7% until one of two things contract noticeably: inflation or the economy.