Home prices have been on a tear since late 2020 despite generally higher rates in 2021. In the past few months, rates have upped the ante by surging at one of the fastest paces in history. But in data just released this week, home prices are moving higher at an even faster pace. What's up with that?

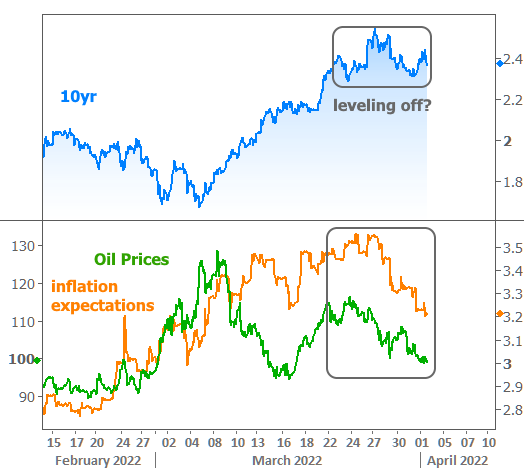

First, let's take a look at rates. We already examined the phenomenon in detail last week, and there were no major changes this week. Actually, the absence of major changes is one of the most promising developments in weeks. As oil prices and inflation expectations have leveled off, rates have attempted to find some sort of ceiling. Whether it's temporary or longer lasting remains to be seen. The following chart shows the leveling-off process in terms of 10yr Treasury yields, which give us a more detailed short term view of rate trends.

Mortgage rates only get one data point per day, so it's much harder to see that they've leveled off a bit this week, but still very easy to see how much they've risen in 2022.

That brings us back to this week's big question: if mortgage rates have moved up so quickly, why are home prices still rising?

There are a few parts to the answer. The first thing we have to consider is the unprecedented supply/demand environment in the housing market combined with a surge in incomes, not to mention the chain reaction of people being able to sell their homes for much higher values who then can spend more on their next home. Housing economists will be sorting these variables out for years, but the point is that there's more to home prices than rates.

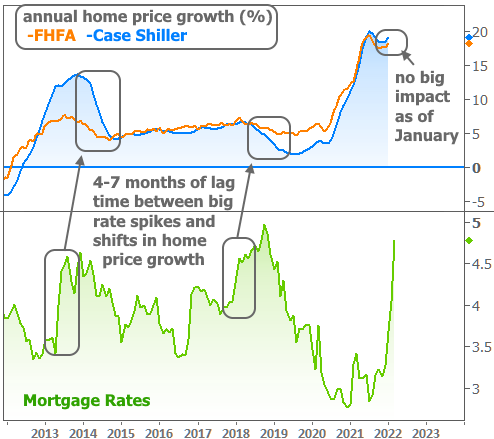

Even so, we can arguably see a few instances of big, unexpected rate spikes resulting in slower home price growth.

The chart also provides 2 clues as to why home price growth was able to accelerate in January. The first clue is the lag time between mortgage rate spikes and the potential impact on prices. It has taken between 4 and 7 months to make it into the data in the past. The second clue is that the major home price indices are fairly backward looking in that we just got January's numbers on March 29th.

Does this mean that current home prices are a ticking time bomb, set to decline in a few months?

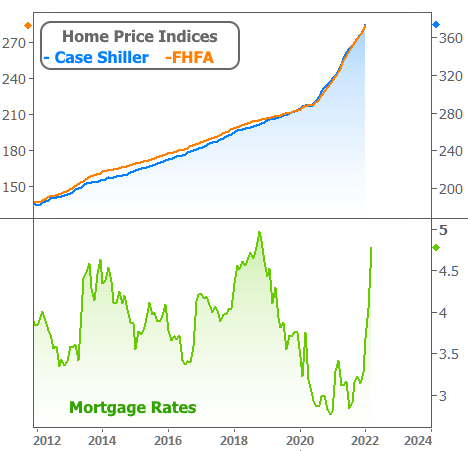

No one knows, actually, and the chart above says nothing about home prices declining. The chart above is the RATE OF CHANGE in prices. If the blue/orange lines are above zero, prices are rising. Here's what the same data looks like if we use the actual home price indices:

In other words, prices have done nothing but move up for more than a decade, regardless of rate volatility. Could that change in the future? Sure, but also, it might not! The only thing most experts agree on is that the 18-20% per year gains will be subsiding.

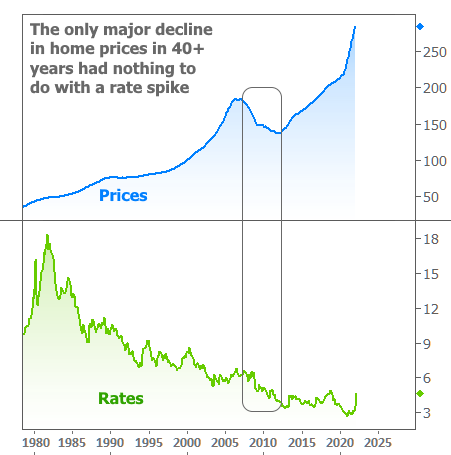

Have home prices ever gone down?

Yes, ask anyone who owned real estate during the financial crisis. But that was actually the only major instance of falling property values in 40+ years, and it had nothing to do with rising rates.

Bottom line: the recent rate spike will almost certainly contribute to a slower pace of home price growth, but it remains to be seen if prices will actually decline. One thought provoking question for those of you who were tuned in to the property market during the financial crisis is this: if you told the average buyer in 2005-2007 and 2020-2022 that their home would lose 20% of its value over the next few years, who would care more? This isn't to say that home prices are invincible, simply that the market dynamics (and underlying loan program availability) are quite different compared to the financial crisis.

Next Wednesday brings the release of the "minutes" from the most recent Fed meeting. With the Fed's policy outlook being one of the key reasons for the abrupt nature of 2022's rate spike, markets are curious to see if the minutes will offer any new insight to the Fed's potential course of action. In addition, trading is often more volatile (for better or worse) in the first few days of a new quarter. As such, by the end of the week, we should have a much better idea of whether rates are indeed serious about leveling off.