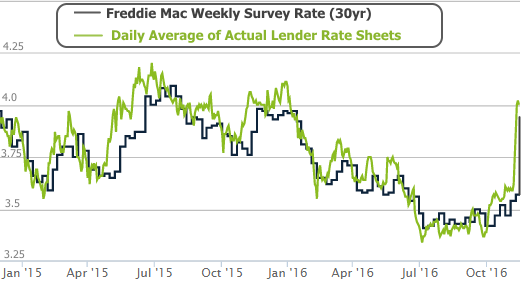

Political fallout aside, the election has really shaken up financial markets. While the evening news is more apt to focus on the stock market recovery, it's getting harder and harder to ignore the destruction of 2016's low mortgage rates. Even the slower-to-react Freddie Mac rate survey caught up with the reality we'd already discussed last week.

Clearly, the election was a catalyst, but why, exactly, are rates responding like this and what are the chances they can come back?

For bond markets (which dictate rates), the issue with the election isn't so much about who won, but rather, the widespread consensus that the other candidate would win. Markets LOVE to price-in as much of the future as they can reasonably foresee. With Clinton, that future was seen as a relative status quo.

The Trump victory started a scramble. Investors were left to guess what Trump's actual policy path might look like and what the effects would be on financial markets. One of the most prevalent conclusions last week was that the election made a Fed rate hike more likely, which was in turn pushing mortgage rates higher.

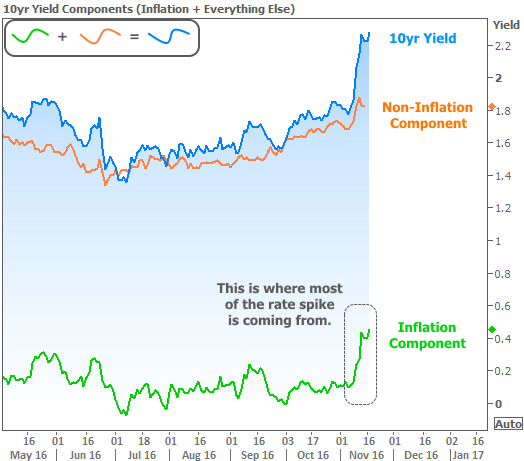

Although Fed rate hike expectations have moved up a bit, they certainly don't account for the move seen in longer term rates. This is plain to see in the following chart (10yr yield is a benchmark for longer-term rates, like mortgages).

If not Fed fears, then what other insidious enemy has bond markets so scared? There are actually several. These include any number of the following (in order of importance and apparent level of certainty):

- Together with a unified GOP congress, Trump is expected to create inflation through increased infrastructure spending, protectionist trade policies, and lower taxes. (Lower taxes + higher spending = the need to print more Treasury debt, or plain old growth. Both would push rates higher. Protectionist policies could raise the cost of imports, which could add to inflation).

- The infrastructure spending possibilities and potential tax cuts have boosted equities markets. Some investors think this is an opportunity to get out of bonds and back into stocks.

- All of the above increases the likelihood that the Fed will hike rates in December. This was already assumed, but now more so. Many investors think the domestic situation makes December a perfect opportunity for Europe to announce that it will taper its asset purchases (thus decreasing overall demand in bond markets, which is bad for rates).

- While it may not have been anything more than a hollow campaign threat, Trump did mention the possibility of "renegotiating" with America's creditors, which is never good for interest rates.

- While it may also have been a rhetorical threat, if Trump were to follow-through on mass-deportation goals, that could have an inflationary effect, as it implies an increase in the cost of labor.

With the exception of the modest increase in Fed rate hike odds, the overwhelmingly unified theme here is inflation. In general, rates will rise for a few key reasons: lower credit quality, stronger growth prospects, and higher inflation expectations. Of those three, inflation has vastly more power to rock rates' world, especially when inflation expectations suddenly change based on fiscal or monetary policy.

If we strip out the inflation component of 10yr yields and isolate it on a chart with the non-inflation-related components, everything becomes clear.

Keep in mind, of course, that this rate spike is made worse by the level of uncertainty over the ultimate policy path. Bond markets have to account for a wider range of risks, and it's much safer for bond traders to be overly defensive of the worst-case scenario until it can be ruled out.

In the coming weeks, to whatever extent such a scenario can be ruled out (or even toned down), we could see rates ease back a bit. But until that happens, take a cue from bond traders: expect the pain to continue until it stops. Don't try to catch the falling knife. The chance of timing it right isn't worth the risk of losing a digit (on your hand or on rate sheets).

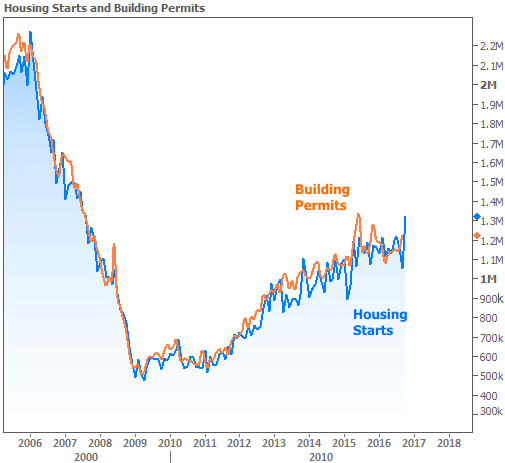

While we ponder rates' fate, why not add a layer of concern by asking ourselves what a surge in rates would mean for the housing market. It was hard not to wonder about such things after this week's impressive surge to 9yr highs in Housing Starts. The past few reports are just now starting to break the stagnant trend from 2015 to mid-2016, and even though rates aren't the final word for residential construction, a sustained rate spike will make it hard to build on the exciting new trends.