The Office of Comptroller of the Currency (OCC) reported on Monday that mortgage performance continued to improve during the third quarter. Both rates of delinquency declined as did foreclosure activity. Delinquency, however, varied considerably among loan types. The OCC Mortgage Metrics Report covers a portfolio of 21.8 million loans with $3.7 trillion in unpaid balances - 42 percent of all first mortgages outstanding in the U.S. Seven-seven percent of the loans are considered prime mortgages with 10 percent or less each of Alt-A, sub-prime, and "other" products.

At the end of the third quarter 93.9 percent of all mortgages held in the portfolios of reporting banks were current and performing, up from 93.0 percent in the second quarter. Mortgages that were 30 to 59 days past due made up 2.3 percent of the portfolio while seriously delinquent loans - those 60 days or more past due or held by bankrupt borrowers whose payments are 30 days or more past due in bankruptcy - accounted for 2.6 percent, down 16.1 percent from the third quarter of 2014 and a slight improvement from the second quarter of this year.

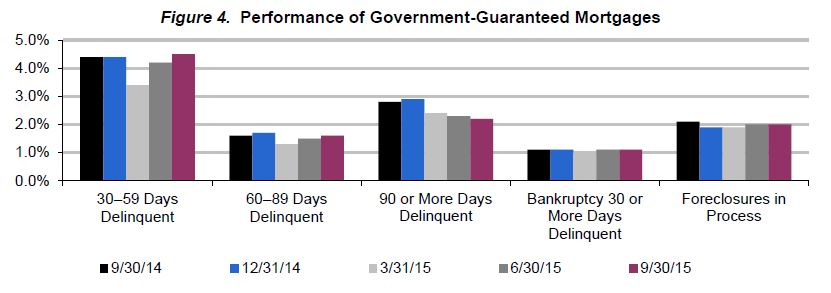

There was significant variation between the performance of Freddie Mac and Fannie Mae (the GSEs) owned/guaranteed mortgages and those that are government guaranteed. Early stage delinquencies for the GSE mortgages were running slightly above 1 percent while loans that are government guaranteed have an early delinquency rate above 4 percent. This pattern holds throughout the various states of non-performance.

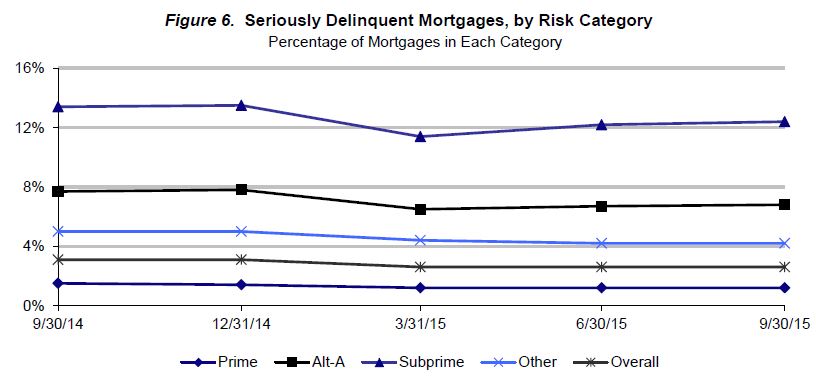

Levels of delinquency among prime and "other" loans have changed little in recent quarters, with prime loans running a 1.2 percent rate in the third quarter compared to 1.5 percent a year earlier. "Other "loans are currently at 4.2 percent, down from 5.0 percent. Despite the small change in the rates of delinquency these numbers represent a 19.9 percent decrease for prime loans and 15.7 percent for other loans.

Delinquencies among Alt-A and subprime loans remain elevated and are not declining as rapidly as the first two categories of loans. Subprime loans have a current rate of 12.4 percent, down 7.5 percent from a year earlier while Alt-A loan delinquencies have decreased year-over-year by 11.2 percent to a rate of 6.8 percent.

In the area of foreclosure activity, reporting servicers initiated 64,156 new foreclosures during the third quarter, down from 82,668 a year earlier. The number of mortgages in the process of foreclosure at the end of the third quarter of 2015 was 269,751, a decrease of 23.8 percent from a year earlier. The percentage of mortgages within this portfolio that were in the process of foreclosure at the end of the third quarter of 2015 was 1.2 percent.

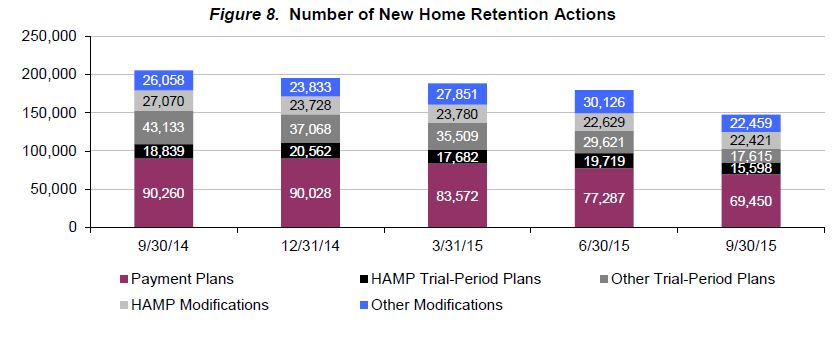

While the need for loss mitigation has declined as mortgage performance improved OCC reports there is still substantial activity on that front. Servicers implemented 147,543 home retention actions during the quarter-including modifications, trial-period plans, and shorter-term payment plans. Nearly 88 percent of modifications made during the third quarter of 2015 reduced monthly principal and interest payments and those reductions averaged $243 per month.

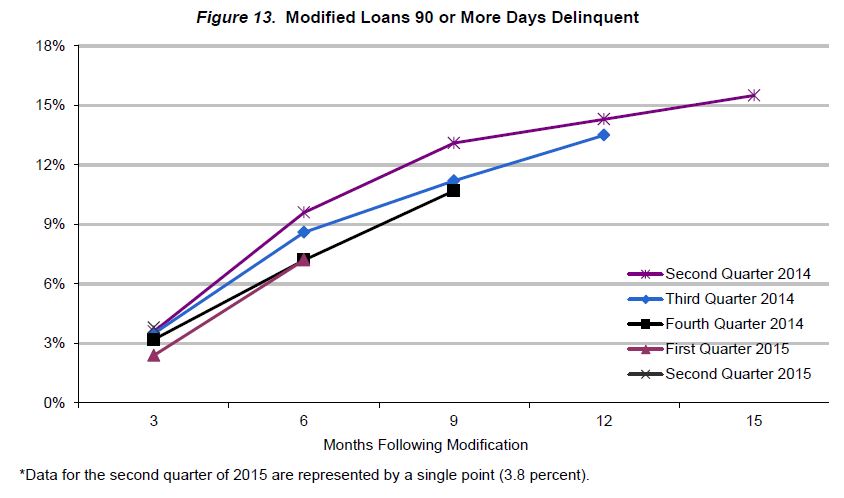

All told there were a total of 3.8 million modifications implemented by servicers between January 1, 2008, and June 30, 2015 and nearly 51 percent of these modifications remained active at the writing of this report. The others had exited the portfolio through payment in full, involuntary liquidation, or transfer to a non-reporting servicer. Of the 1,922,661 active modifications at the end of the third quarter of 2015 71.2 percent were current and performing, 23.6 percent were delinquent, and 5.2 percent were in the process of foreclosure.