Jumbo refinances led the way as mortgage fraud risk posted another gain in the second quarter of 2017. CoreLogic reports that overall risk, as measured by its Mortgage Application Fraud Risk Index, was up 16.9 percent from the second quarter of 2016. The company estimates 13,404 mortgage applications contained indications of fraud, an 0.82 percent incidence, compared to 12,718 applications or 0.70 percent a year earlier.

CoreLogic's Mortgage Fraud Report analyzes the collective level of loan application fraud risk the mortgage industry is experiencing each quarter. The report looks at detailed data for six fraud type indicators that complement the national index: identity, income, occupancy, property, transaction, and undisclosed real estate debt.

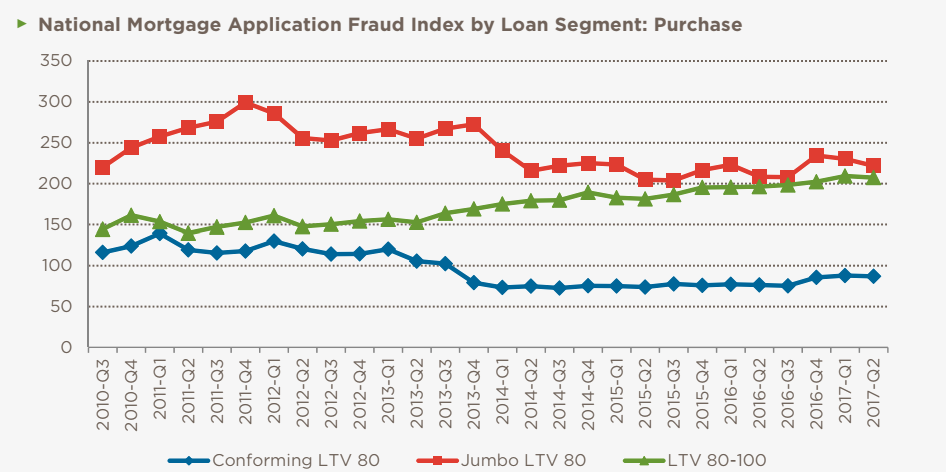

The company said the continued shift from a refinance heavy market to one in which purchase mortgages predominate is a key factor in the national increase. Purchase applications have a higher risk because of the stronger motivations and increased opportunities for fraud as well as the numbers of parties engaged in the transaction.

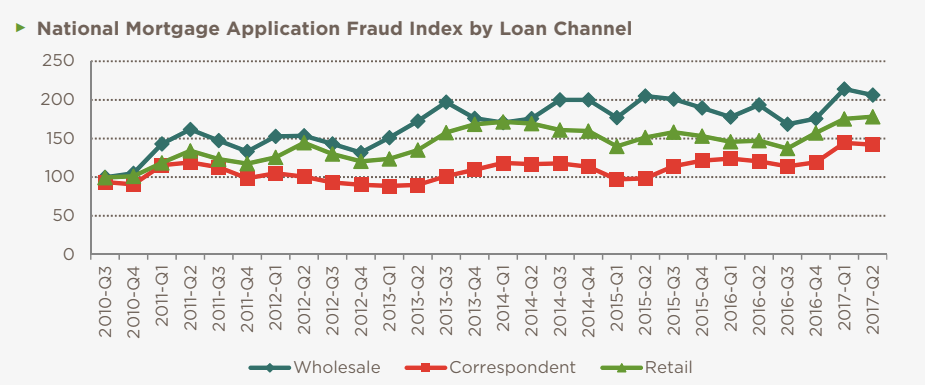

A second factor was the increase from 5.0 percent to 7.3 percent in the share of loans originated through wholesale channels, a 48 percent change. Wholesale applications have traditionally shown a higher risk level than those in the retail channel.

"This past year we saw a relatively large increase in the CoreLogic National Mortgage Application Fraud Index," said Bridget Berg, principal, Fraud Solutions for CoreLogic. "If the factors that influenced the increase continue, including a shift to purchase transactions and growing wholesale channel origination activity, it is likely that mortgage application fraud risk will continue to rise as well. Fraud on cash-out refinance transactions and home equity loans may become more of a factor in the coming years as home values and equity rise."

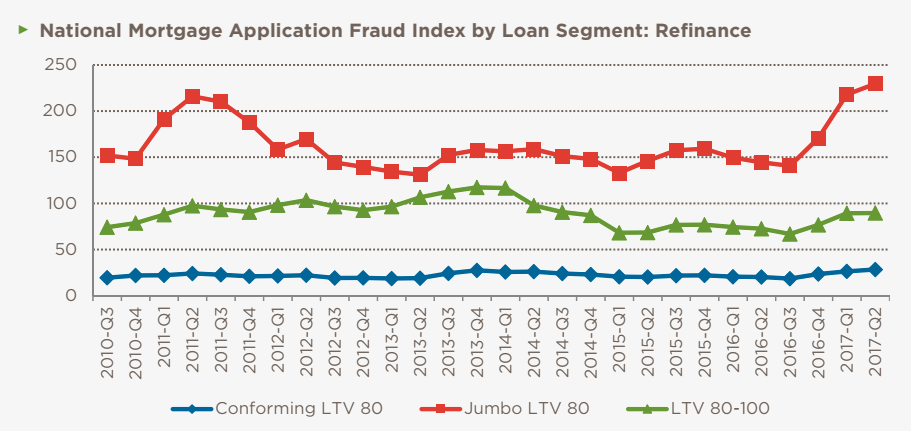

While purchase transactions account for most of the increase in the national fraud index, the refinance segments moved higher, most notably in the Jumbo segment which risk increased by 59 percent even as application volumes fell by 35 percent. Specific risk areas for jumbo refinances included rapid refinancing after purchase, values not supported by market changes, and occupancy red flags.

Florida, which held the top position vis-à-vis the level of application fraud risk for three years dropped to third place after a 3 percent decrease, supplanted by New York State followed by New Jersey. CoreLogic says that, because application volumes in Florida are 2.5 times that of either New York or New Jersey, all three states bear watching.

States with the greatest growth in risk include Iowa, Indiana, Missouri, Louisiana and Idaho. Although they have the highest growth in risk, the four of these states (Louisiana is ranked number 8) are still outside the top 25 in terms of overall risk.

Occupancy fraud risk, which occurs when mortgage applications deliberately misrepresent their intended use of the property (primarily falsely claiming owner occupancy), had the greatest increase among indicators, 7.0 percent.

Transaction fraud, when the nature of the transaction is misrepresented, such as an undisclosed agreement between parties, straw buyers, or falsified down payments, increased 3.9 percent year over year.

Income fraud was up 3.5 percent, with much of the change coming in the last half of 2016. This type of fraud includes misrepresentation of the existence, continuation, source or amount of income used to qualify for a mortgage.

There was a 7.3 percent drop in the incidence of identity fraud risk, while undisclosed real estate debt and property fraud risk (misrepresenting information about a property or its value) both were down, by 2.7 percent and 1.9 percent respectively.

A final category is multi-closing fraud which CoreLogic calls an extremely profitable scam. It takes advantage of the lag between closing a loan and recording its documents to solicit multiple loans on a single property. There was a spike in this type of fraud in 2014, then a decrease the next two years as lenders utilized CoreLogic's alert program. However, the company says it expects an increase this year.

The CoreLogic Mortgage Application Fraud Risk Index represents the collective level of fraud risk the mortgage industry is experiencing based on the share of loan applications with a high risk of fraud. The index is standardized to a baseline of 100 for the share of high-risk loan applications nationally in the third quarter of 2010. Each 1-point change in the index represents a 1-percent change in the share of mortgage applications having a high risk of fraud.